By 2026, numerous changes are set for Australia’s retirement savings system. Australians have long relied on superannuation as a key wealth-building tool, supported by highly favourable tax concessions. However, new legislative updates—particularly the introduction of Division 296 tax—are reshaping how high superannuation balances are treated.

These changes are significant and signal a shift in how the government views large super balances. From July 2026, tax concessions will be more “targeted,” especially for individuals with superannuation balances exceeding $3 million. This makes the reforms especially important for retirees and those approaching retirement, as they now play a crucial role in estate and financial planning.

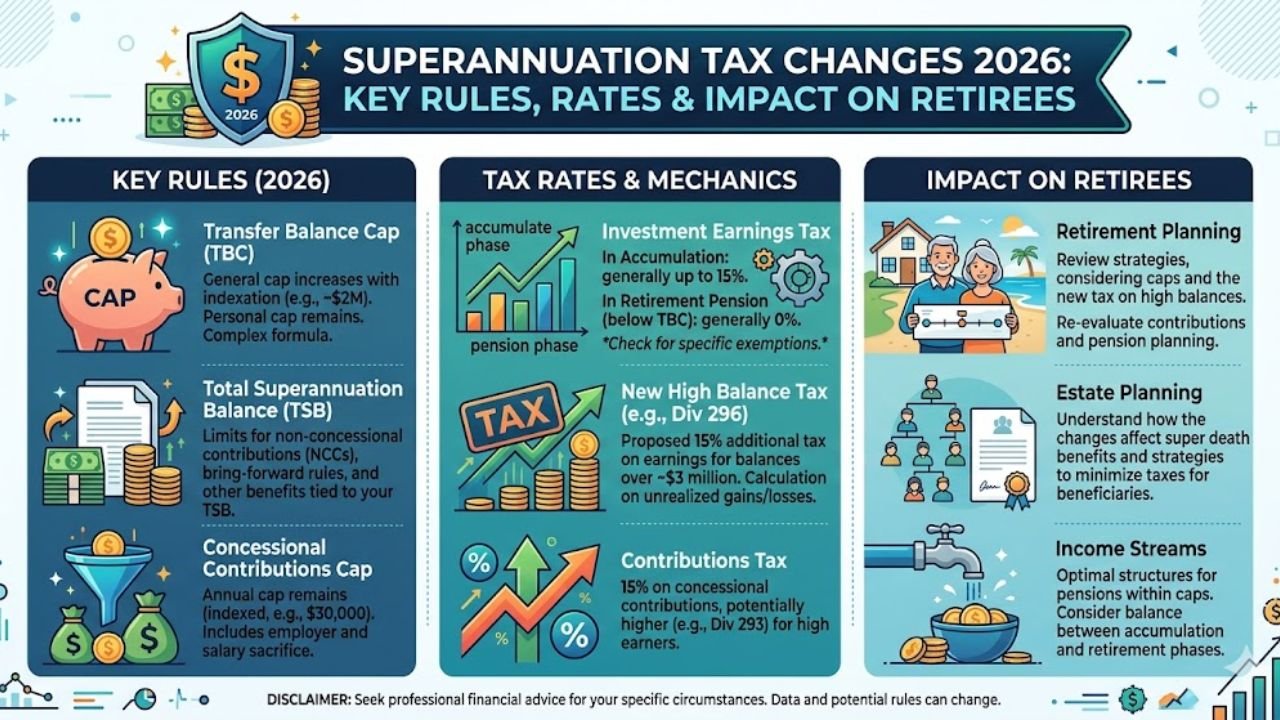

What is the New Division 296 Tax Framework?

The most discussed reform is the Division 296 tax, which introduces additional taxation on superannuation earnings for high-balance individuals. Starting July 1, 2026, a layered tax system will apply to reduce the level of government support for large super accounts.

Previously, earnings in the accumulation phase were taxed at a flat 15%, while retirement phase earnings were often tax-free. Under the new rules, individuals with balances above $3 million will pay an additional 15% tax on a portion of their earnings.

For those with balances exceeding $10 million, an extra 10% tax applies—bringing the total effective tax rate on those earnings to 25% or more when combined with existing fund taxes. This reform aims to ensure superannuation remains a retirement vehicle rather than a tax shelter for extreme wealth.

Key Thresholds and Contribution Rates for 2025–2026

The Australian Taxation Office (ATO) sets specific thresholds and contribution caps that are essential for planning under the new system.

Superannuation Guarantee (SG) rate: 12%

Concessional contribution cap: $30,000

Non-concessional contribution cap: $120,000

Bring-forward rule: up to $360,000 over three years

These limits are indexed to wage growth and inflation, making them critical tools for managing total super balances ahead of Division 296 implementation in the 2026–27 financial year.

Metric

2025–2026

2026–2027 (Estimated)

Superannuation Guarantee

12.0%

12.0%

Concessional Cap

$30,000

$32,500

Non-Concessional Cap

$120,000

$130,000

Transfer Balance Cap

$2,000,000

$2,100,000

Division 296 Threshold

N/A

$3,000,000

Very High Threshold

N/A

$10,000,000

Impact on Retirees with Over $3 Million

The $3 million threshold introduces a new category of “high-balance” retirees. Importantly, the additional tax does not apply to the entire balance—only the portion exceeding the threshold.

For example, if a retiree holds $4 million in super, only the earnings on the $1 million above the threshold are subject to the additional 15% tax. However, calculating this requires careful tracking of total superannuation balances across multiple accounts.

A major relief for investors is that the final legislation excludes unrealized capital gains. Only realized earnings—such as dividends, interest, and rental income—are taxed. This is particularly beneficial for those holding illiquid assets like property.

Strategic Adjustments and Cost Base Reset

As July 2026 approaches, strategic planning becomes essential. One key option is the cost base reset election, allowing eligible individuals to reset asset values to market value as of June 30, 2026.

This one-time opportunity ensures that future tax calculations only apply to gains made after the new rules take effect, protecting historical growth from additional taxation.

Additionally, many couples are exploring contribution splitting strategies to balance their super accounts. By distributing funds between spouses, families can potentially keep both balances below $3 million, maximizing access to lower tax rates.

The Future of Superannuation Policy

The 2026 reforms reflect a broader shift toward sustainability in Australia’s retirement system. While the government estimates only 0.5% of Australians will be directly affected, the additional revenue is intended to support the long-term viability of the Age Pension and other services.

For most workers, the increase in the SG rate to 12% and higher contribution caps will support more comfortable retirements. However, high-net-worth individuals will need to move beyond the “set and forget” approach and actively manage their super strategies.

Professional financial advice, portfolio restructuring, and tools like family trusts and transfer balance caps (projected to reach $2.1 million) will become increasingly important under the new system.

FAQs

Q1 Does the new 15% tax apply to my entire super balance?

No. The tax only applies to the portion of your super balance above $3 million, and only to the corresponding share of earnings.

Q2 What is the cost base reset?

It is an optional rule allowing eligible individuals to reset asset values to their market value as of June 30, 2026. This ensures only future gains are taxed under the new framework.

Q3 Will the $3 million threshold increase over time?

Yes. The threshold will be indexed to inflation, though increases will occur in fixed increments rather than annually.